Automating your savings is an effective strategy for building wealth and achieving financial goals without the need for constant monitoring. By setting up automatic transfers from your checking account to your savings account, you can streamline your financial management and ensure consistent savings. This article explores the benefits of automating savings and provides a step-by-step guide to setting it up.

Benefits of Automating Your Savings

Consistency in Saving

One of the primary benefits of automating your savings is consistency. By scheduling regular transfers, you ensure that a portion of your income is consistently saved each month. This approach removes the need for manual intervention and helps establish a routine of saving.

Moreover, automating savings eliminates the temptation to spend the money instead. Since the transfer happens automatically, you are less likely to divert funds from your savings to other expenses.

Reduced Stress and Time Savings

Automating your savings reduces the stress associated with managing finances. Once the setup is complete, you don’t need to worry about remembering to transfer funds manually. Hence, it simplifies your financial management and frees up time for other activities.

Furthermore, automated savings eliminate the need for constant tracking and decision-making regarding savings. This streamlined process allows you to focus on other aspects of your financial plan without the burden of manual transfers.

Encouragement of Financial Discipline

Automatic transfers foster financial discipline by making saving a non-negotiable part of your routine. As funds are transferred automatically, you adjust your spending around the remaining balance in your checking account. This adjustment encourages better budgeting and financial planning.

Additionally, setting up automatic savings helps prioritize your savings goals. By treating savings as a fixed expense, you ensure that you meet your financial objectives, such as building an emergency fund or saving for retirement.

How to Set Up Automated Savings

Choose the Right Savings Account

Before setting up automated savings, select a savings account that suits your needs. Consider factors such as interest rates, account fees, and accessibility. High-yield savings accounts or online savings accounts often offer better interest rates compared to traditional savings accounts.

Moreover, ensure that the account you choose aligns with your financial goals. For example, if you are saving for a short-term goal, a high-yield savings account may be ideal. Conversely, if you are saving for retirement, you might consider an account with tax advantages.

Determine Your Savings Goals

Define your savings goals and determine how much you want to save each month. Having clear goals helps you set a realistic savings amount and ensures that your automated transfers align with your financial objectives.

For instance, if you are saving for an emergency fund, calculate the total amount needed and divide it by the number of months until you reach your goal. Similarly, if you are saving for a vacation or a large purchase, estimate the required amount and set a target date.

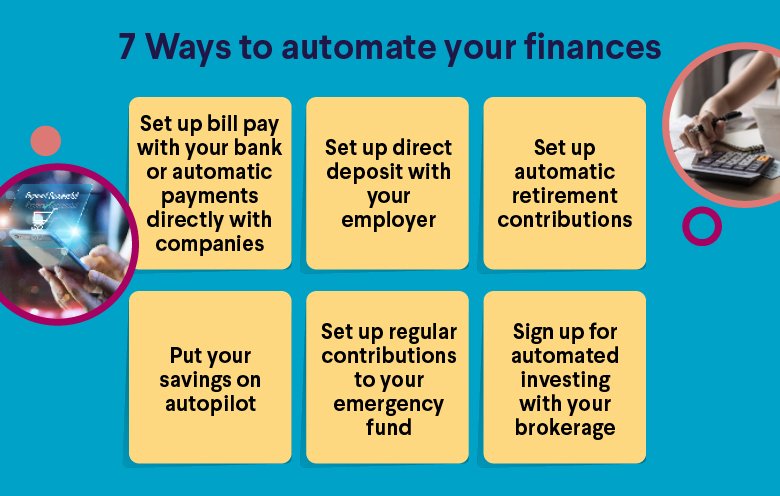

Set Up Automatic Transfers

Most banks and financial institutions offer online banking services that allow you to set up automatic transfers. Follow these steps to establish automatic savings:

- Log In to Your Online Banking Account: Access your bank’s online banking platform or mobile app.

- Navigate to the Transfer Section: Locate the section for setting up transfers or automatic payments.

- Select Accounts: Choose the account you want to transfer funds from (typically your checking account) and the account you want to transfer funds to (your savings account).

- Specify Transfer Details: Enter the amount you want to transfer and the frequency (e.g., weekly, bi-weekly, or monthly).

- Review and Confirm: Review the transfer details and confirm the setup. Ensure that the transfers are scheduled according to your preferences.

Monitor and Adjust

After setting up automated savings, periodically review your accounts and financial goals. Monitor your savings progress and make adjustments as needed. For example, if your financial situation changes or you achieve a savings goal, you may need to increase or decrease your automated transfers.

Additionally, check for any changes in account fees or interest rates that might affect your savings. Regularly reassessing your automated savings plan ensures that it remains effective and aligned with your financial goals.

Common Pitfalls to Avoid

Overdraft Risk

Ensure that you maintain a sufficient balance in your checking account to cover the automatic transfers. Overdrafts can result in fees and disrupt your savings plan. To avoid this, monitor your account balance and set up alerts to track your financial activity.

Setting Unrealistic Goals

Be realistic about the amount you can comfortably save each month. Setting overly ambitious savings goals may strain your budget and lead to frustration. Start with a manageable amount and gradually increase it as your financial situation improves.

Neglecting to Review

Failing to review your automated savings plan can lead to missed opportunities for optimization. Regularly check your progress and make adjustments based on changes in your financial situation or goals.

Conclusion

In conclusion, automating your savings offers numerous benefits, including consistency, reduced stress, and enhanced financial discipline. By choosing the right savings account, setting clear goals, and establishing automatic transfers, you can streamline your financial management and achieve your savings objectives.

Regularly monitoring and adjusting your savings plan ensures that it remains effective and aligned with your financial goals. Embrace the convenience of automated savings to build wealth and achieve financial security with minimal effort.